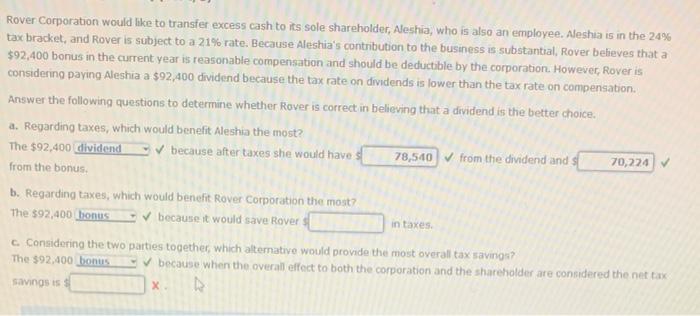

Old-fashioned Finance & Strange Loans: What’s the Improvement?

Regardless of whether you’re purchasing your earliest house otherwise the last household, all the resident will have to address the fresh new overwhelming concern: Just what mortgage perform We prefer?

The first step you can bring is always to discover a few earliest mortgage brokers, antique and you will strange. One another loan items gets their unique positives and negatives in order to the brand new borrower.

Preciselywhat are Traditional Funds?

Old-fashioned funds are not secure of the a professional authorities system instance brand new Government Homes Government (FHA), Service from Agriculture (USDA) or Agencies regarding Veterans’ Circumstances (VA). As an alternative, these include provided by individual loan providers and certainly will essentially go after more strict criteria compared to other mortgage sizes.

They have been good for consumers whom actually have expert borrowing. When you are currently at good economic status and can render a much bigger down-payment, the procedure shouldn’t be burdensome for your. Though it is hard to be eligible for that it financing style of, you’ll find advantages such as for instance independency in terms of assets that you could get and possible opportunity to somewhat decrease your home loan insurance rates.

To get they in the layman’s words fixed-rate mortgages will have an interest rate one never transform. In the event your residence taxes beginning to increase otherwise your own homeowners’ advanced grows, the fresh new payment per month for the loan will always be an identical. If you find yourself an individual who is used to help you structure, that it loan sorts of may possibly provide your that have balance and peace out-of head.

Additionally, it is prominent for many who is actually paying down right down to grab demand for a remedy-ranked financial. You will probably find you to definitely a 30 otherwise 15-seasons fixed-price home loan is the perfect fit for your. Overall, your choice to go with a predetermined-rates home loan may come out of your newest items or coming preparations.

Normally, homeowners exactly who plan on transferring in the future often incorporate for a varying rates mortgage. They truly are often swayed of the sparkling function of getting a diminished rate of interest right off the bat. To phrase it differently, your payment can begin regarding more affordable.

Very necessary hyperlink very first-day homebuyers otherwise younger those who are moving forward in their career commonly lean towards the an adjustable rate financial. By doing this, if you decide later that you like to move, you might not end up being tied up down seriously to a particular mortgage sorts of. From inside the basic terminology of experiencing a variable price home loan, you might not have to worry about refinancing. You will also have benefitted regarding a low interest rate.

What exactly are Unconventional Loans?

As previously mentioned prior to, traditional fund wanted increased credit history, straight down obligations-to-earnings proportion and you will big advance payment during the bucks. In certain products, it usually do not continually be accomplished by borrowers. When you’re in this instance, searching into an unusual loan.

For the regard to it’s name, strange finance, vary off very funds. They are supported by the government otherwise safeguarded as a result of a bank otherwise private lender and you will best for those with a lower life expectancy-earnings or poor credit.

The actual only real drawback is inspired by the fact the loan limitation is gloomier, and if you are seeking to a property with high price tag, you may need a much bigger advance payment. Unconventional fund is split into one or two loan systems: FHA funds and Virtual assistant funds.

Should you cannot top quality having a traditional mortgage, you may want to believe a keen FHA mortgage. Since you now understand that an unconventional mortgage try authorities-recognized, you can observe how the financing processes will work. If, any kind of time point, your default in your financing along with your home’s worth try not to cover the quantity, brand new FHA will require more than and you can repay the lending company.

Such purchase will simply occurs as mortgage try covered, it is therefore apparent that there exists smaller restrictions to own FHA money. This also means that your own their lender could probably leave you a decreased down-payment.

The second sorts of strange financing try an experts Points Finance (VA) that must definitely be approved by a loan provider that will be secured of the the brand new U.S. Institution out-of Veterans Affairs (VA). The main purpose of good Virtual assistant financing will be to offer military group and their group with the ability to funds a house.

Are noticed getting an effective Va loan, the individual have to be a working obligations service affiliate, National Shield member or reservists and meet with the service conditions required of the loan. Eventually, the new Va will determine the brand new recognition of the mortgage sorts of.

It is time to Determine

Finally, it might be your responsibility, brand new homeowner, to decide on an informed home loan for your disease. However, that doesn’t mean you cannot found help from the mortgage benefits on Prysma.

If you’re considering a normal financing otherwise a non-traditional financing, Prysma is obtainable whenever you you want united states. Simply call us from the 855-950-0202 or fill in our very own on line software plus one of our support service agencies will get in contact with your.

Recent Comments